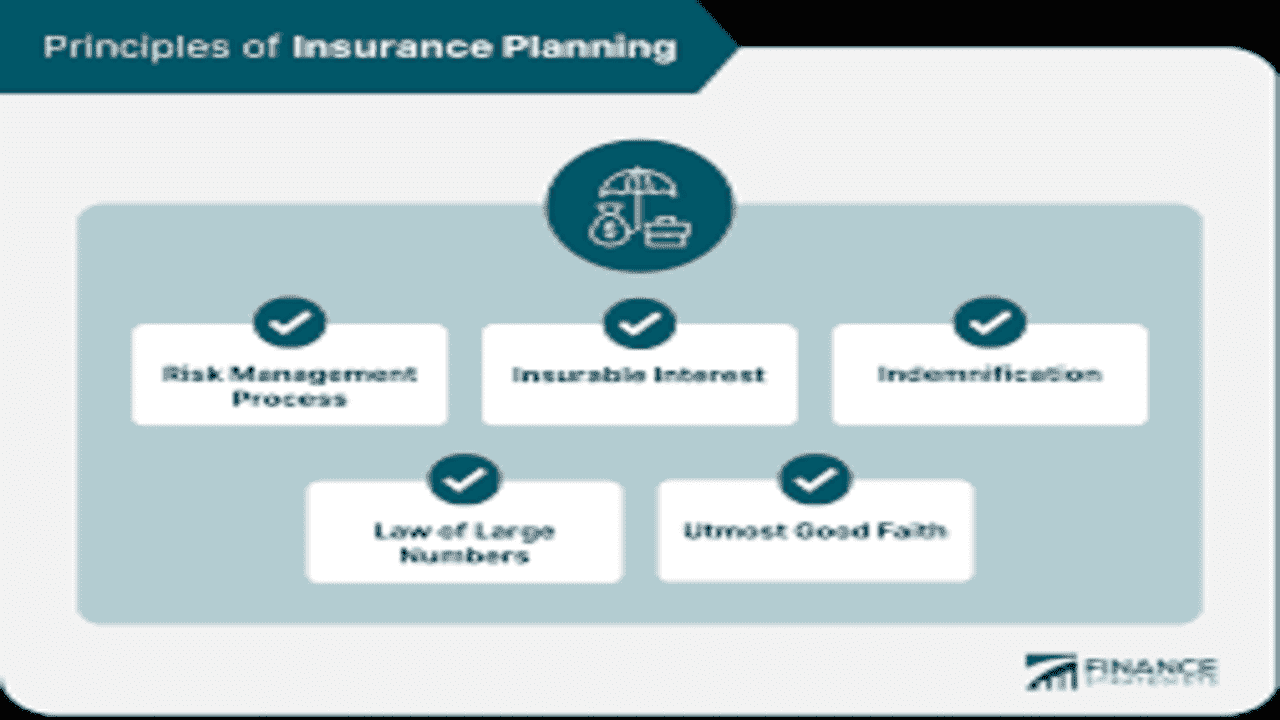

Insurance Planning

Insurance is a critical aspect of financial planning that provides protection against unforeseen events. Effective insurance planning ensures financial stability and peace of mind for individuals and families. By strategically selecting insurance policies, one can mitigate risks and secure their future.

Types of Insurance Policies

Life Insurance

Life insurance offers financial protection to beneficiaries in the event of the policyholder’s death. There are various types of life insurance, including term life, whole life, and universal life, each catering to different needs and preferences.

Health Insurance

Health insurance covers medical expenses incurred due to illness or injury. Individual, family, and Medicare plans are available to suit diverse healthcare needs and budgets.

Property Insurance

Property insurance safeguards assets such as homes, rental properties, and belongings against damages or loss caused by unforeseen events like fires, thefts, or natural disasters.

Auto Insurance

Auto insurance provides financial protection in case of accidents, theft, or damages to vehicles. Liability, collision, and comprehensive coverage options are available to address different risks.

Factors to Consider in Insurance Planning

Financial Goals and Needs Assessment

Evaluate financial objectives and determine the level of insurance coverage required to meet specific needs and goals.

Risk Assessment

Identify potential risks and vulnerabilities to determine appropriate insurance coverage for comprehensive protection.

Budget Allocation

Allocate financial resources efficiently to acquire necessary insurance coverage without compromising other financial goals.

Comparison of Policies

Research and compare insurance policies from different providers to find the most suitable coverage options at competitive rates.

Review and Adjustment

Regularly review insurance policies to ensure they align with changing circumstances and make adjustments as needed.

Strategies for Effective Insurance Planning

Adequate Coverage Determination

Ensure insurance coverage is sufficient to protect against potential risks and adequately meet financial obligations.

Diversification of Policies

Diversify insurance portfolios to spread risks across multiple policies and providers, enhancing overall protection.

Regular Policy Reviews

Periodically review insurance policies to assess coverage adequacy, identify gaps, and make necessary adjustments based on changing needs.

Emergency Fund Establishment

Build an emergency fund to cover unexpected expenses and mitigate the need to rely solely on insurance claims in times of crisis.

Consultation with Professionals

Seek guidance from insurance experts or financial advisors to navigate complex insurance options and make informed decisions.

Common Mistakes to Avoid in Insurance Planning

Underestimating Coverage Needs

Avoid underestimating insurance coverage needs, as inadequate protection may lead to financial strain during emergencies.

Neglecting Regular Policy Reviews

Regularly review insurance policies to ensure they remain relevant and provide adequate coverage as circumstances change.

Not Considering Life Changes

Factor in significant life changes such as marriage, parenthood, or career advancements when reassessing insurance needs.

Ignoring Policy Details

Pay attention to policy details, including terms, conditions, and exclusions, to avoid surprises during claim settlements.

Overlooking the Importance of Deductibles and Co-pays

Consider deductibles and co-pays when selecting insurance policies to strike a balance between premiums and out-of-pocket expenses.

FAQs about Insurance Planning

How do I determine the right insurance coverage for my needs? Determining the right insurance coverage involves assessing individual needs, financial goals, and risk tolerance levels. Consulting with insurance professionals can provide valuable guidance in selecting appropriate coverage options.

Can I have multiple insurance policies covering the same risk? Yes, individuals can have multiple insurance policies covering the same risk, which is known as overlapping coverage. However, it’s essential to avoid over-insuring or duplicating coverage excessively to prevent unnecessary expenses.

Is it necessary to review my insurance policies annually? Yes, reviewing insurance policies annually is crucial to ensure they remain relevant and provide adequate coverage. Life changes, such as marriage, childbirth, or career advancements, may necessitate adjustments to existing policies.

What happens if I miss a premium payment? Missing a premium payment may result in policy lapses or cancellation, depending on the insurer’s policies. Some insurance companies offer grace periods or payment extensions, but it’s essential to communicate with the provider to avoid coverage interruptions.

How does insurance planning change with major life events? Major life events such as marriage, divorce, childbirth, or retirement may impact insurance needs. It’s essential to reassess coverage requirements and make necessary adjustments to ensure adequate protection during transitional phases.

Should I consider insurance as an investment option? While some insurance products offer investment components, such as cash value or dividends, it’s essential to view insurance primarily as a risk management tool rather than an investment. Consultation with financial advisors can help determine the most suitable investment strategies based on individual goals and risk profiles.

Conclusion

Insurance planning plays a vital role in safeguarding one’s financial future against unforeseen events and risks. By understanding insurance options, assessing individual needs, and implementing effective strategies, individuals and families can secure comprehensive protection and achieve peace of mind.

Helpful Sources