What is a grace period on a credit card?

In the whirlwind of financial management, understanding the intricacies of credit cards can be both daunting and essential. Among the many features and terms associated with credit cards, the grace period stands out as a vital component, often shrouded in mystery. Let’s unravel this enigma together as we delve into what a grace period on a credit card truly entails and how it can serve as a boon for savvy consumers.

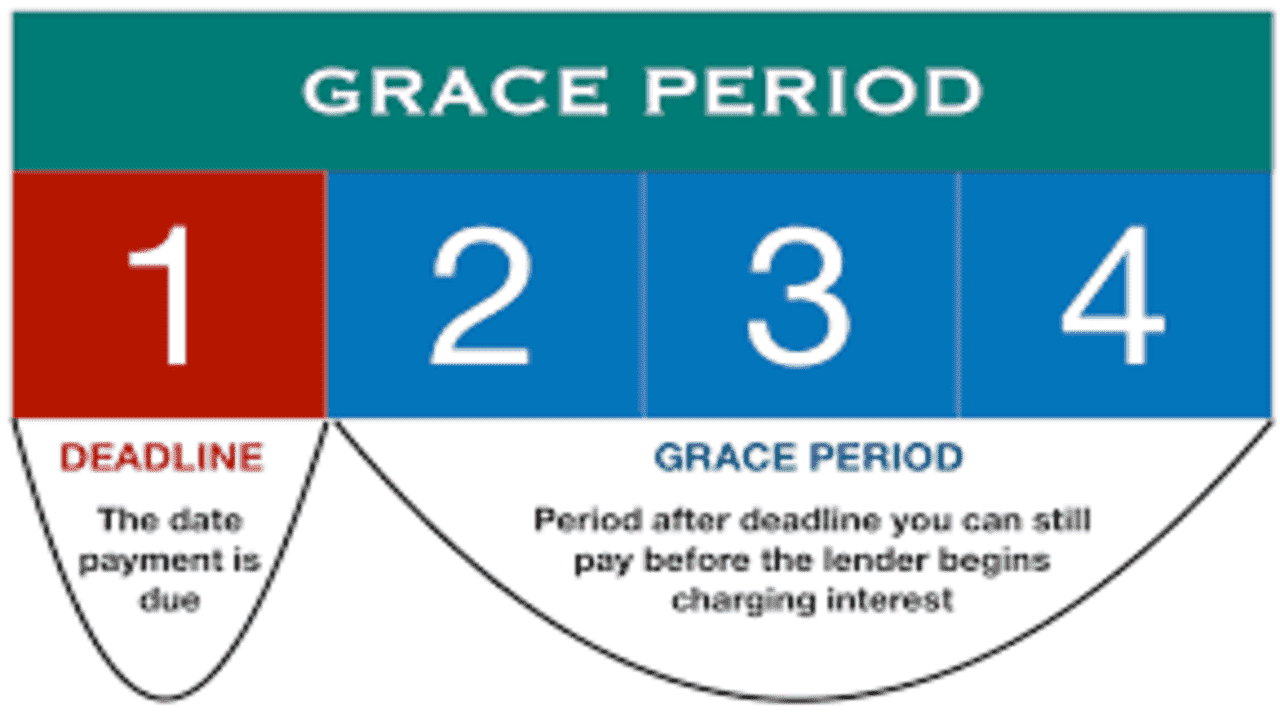

What is a Grace Period on a Credit Card?

A grace period on a credit card is a window of time during which cardholders can make purchases without incurring any interest charges. It typically spans from the end of a billing cycle to the due date for that billing cycle’s payment. Understanding this grace period is pivotal for making informed financial decisions and optimizing the benefits of credit card usage.

Exploring the Mechanics of Grace Periods:

The grace period operates as a buffer between the end of a billing cycle and the due date for payment. During this period, if the entire outstanding balance is paid off, no interest accrues on the purchases made during that billing cycle. Let’s break down the mechanics further:

- How Does the Grace Period Work? The grace period kicks in when the billing cycle ends and extends until the payment due date for that cycle. If the outstanding balance is cleared within this timeframe, no interest is charged on purchases.

- Factors Influencing Grace Periods Several factors can influence the length and availability of a grace period, including the credit card issuer’s policies, the cardholder’s creditworthiness, and the type of transaction.

- Impact of Partial Payments While paying off the entire balance within the grace period ensures no interest accrues, making only a partial payment may trigger interest charges on the remaining balance.

- Utilizing Grace Periods Strategically Understanding the nuances of grace periods empowers cardholders to strategically time their purchases and payments to maximize interest savings and financial flexibility.

Benefits of Grace Periods

- HInterest-Free Borrowing During the grace period, cardholders essentially enjoy interest-free borrowing, provided they pay off the entire balance by the due date.

- Enhanced Cash Flow Management Grace periods facilitate better cash flow management by offering a window to settle outstanding balances without incurring additional costs.

- Financial Planning Flexibility The flexibility afforded by grace periods allows individuals to align their financial planning with their income streams and expenditure patterns.

- Opportunity for Rewards Optimization By leveraging grace periods effectively, cardholders can optimize their rewards programs and capitalize on benefits such as cashback or travel miles.

Common Misconceptions

- Grace Periods Equal Payment Due Dates Contrary to popular belief, the grace period extends beyond the payment due date, providing an opportunity to settle balances without incurring interest.

- Grace Periods Apply to All Transactions While grace periods are common for purchases, they may not necessarily apply to other transactions like cash advances or balance transfers, which often accrue interest from the date of the transaction.

- Length of Grace Periods Grace periods can vary significantly among credit card issuers and even among different card products offered by the same issuer.

- Impact of Interest Rates Although grace periods offer interest-free borrowing, the interest rates applicable after the grace period can significantly impact the overall cost of credit card usage.

FAQs (Frequently Asked Questions):

- What happens if I don’t pay my balance in full during the grace period? If the entire balance is not paid off during the grace period, interest charges will accrue on the remaining balance, increasing the overall cost of credit.

- Can I request an extension on my credit card’s grace period? Grace periods are typically predefined by the credit card issuer and may not be subject to extension requests. It’s essential to review the terms and conditions of your credit card agreement for clarification.

- Do all credit cards offer grace periods? While grace periods are a common feature of many credit cards, not all cards may offer this benefit. It’s advisable to confirm the presence and terms of the grace period with your card issuer.

- Does utilizing the grace period affect my credit score? Utilizing the grace period responsibly by paying off balances in full can reflect positively on your credit utilization ratio and, consequently, your credit score.

- Can I make payments during the grace period? Yes, making payments during the grace period is permissible and can help reduce the outstanding balance, minimizing interest charges.

- Is there a penalty for missing the grace period deadline? Missing the grace period deadline may result in late payment fees and potentially impact your credit score. It’s crucial to adhere to payment deadlines to avoid such consequences.

Conclusion:

In the realm of credit card management, understanding the nuances of grace periods is akin to wielding a powerful tool for financial empowerment. By leveraging this window of opportunity effectively, cardholders can navigate the credit landscape with confidence, optimizing benefits while minimizing costs. As you embark on your financial journey, may the insights gleaned from this guide serve as a compass, guiding you towards prudent decision-making and fiscal well-being.